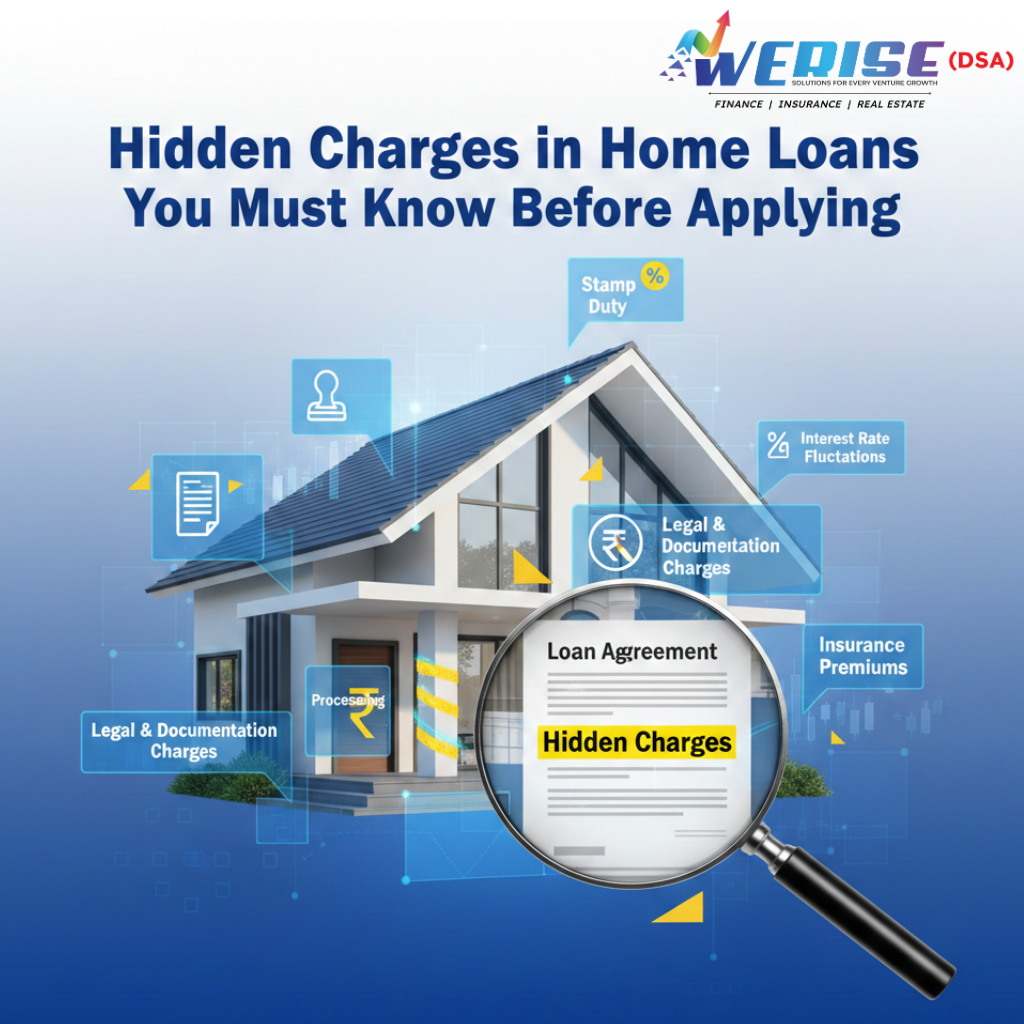

When applying for a home loan, most borrowers focus only on the interest rate and EMI. But what many don’t realize is that hidden charges can significantly increase the total cost of your home loan—sometimes by lakhs of rupees over the loan tenure.

In this guide, WERISE DSA explains the hidden charges in home loans you must know before applying, so you can make an informed and cost-effective decision.

Why Understanding Hidden Charges Is Important

Even a home loan with a low interest rate can become expensive if you ignore additional fees. Knowing these charges helps you:

- Compare lenders accurately

- Avoid surprises after sanction

- Plan your finances better

- Negotiate effectively

1. Processing Fees

This is one of the most common home loan charges.

- Usually 0.25% – 1% of the loan amount

- Some banks offer waivers during festive offers

Example:

For a ₹50 lakh loan, 1% = ₹50,000

Always ask if the processing fee is negotiable or refundable.

2. Legal & Technical Verification Charges

Before approving your loan, lenders verify:

- Property title & ownership

- Building approvals

- Layout plans

These checks involve:

- Legal fees

- Technical valuation fees

These charges are non-refundable, even if the loan is rejected.

3. Property Valuation Charges

Banks appoint valuers to assess the market value of the property.

- Charged separately or bundled

- Depends on property type & location

The bank’s valuation may be lower than the purchase price, affecting loan eligibility.

4. Stamp Duty & Registration Charges

These are not included in the loan amount and must be paid by the borrower.

- Stamp duty: 5–7% (varies by state)

- Registration charges: ~1%

Many first-time buyers forget to budget for this.

5. Conversion Charges (Fixed to Floating / Vice Versa)

If you want to switch your interest rate type later:

- Banks may charge 0.5% – 1% of outstanding loan

- Often applicable when converting from fixed to floating

Ask upfront if your lender allows free conversion.

6. Prepayment & Foreclosure Charges

Many borrowers plan to close their loan early—but:

- Some lenders charge penalties on prepayment

- Floating-rate loans usually have no foreclosure charges

- Fixed-rate loans may still attract penalties

Always read prepayment terms carefully.

7. Late Payment & EMI Bounce Charges

Missing EMIs can be costly:

- Late payment fees

- EMI bounce charges

- Negative impact on CIBIL score

- Even a single missed EMI can increase future loan costs.

8. Documentation & Administrative Charges

Some lenders include:

- Documentation fees

- Account maintenance charges

- Statement or certificate fees

These may seem small but add up over time.

9. Insurance-Related Charges (Often Misunderstood)

Banks may offer:

- Home loan protection insurance

- Property insurance

These are optional, but sometimes bundled into the loan without clear explanation.

Always ask:

✔ Is insurance mandatory?

✔ Is it single premium or yearly?

10. Balance Transfer & Top-Up Charges

If you plan to:

- Transfer your loan to another bank

- Take a top-up loan

There may be:

- Processing fees

- Legal & valuation charges again

Evaluate total savings before switching.

How to Avoid Hidden Home Loan Charges

✔ Read the sanction letter carefully

✔ Ask for a complete fee breakup

✔ Compare multiple lenders

✔ Negotiate charges wherever possible

✔ Apply through a trusted DSA

Why Choose WERISE DSA for Home Loans?

At WERISE DSA, transparency comes first.

What You Get with WERISE DSA:

✅ Clear explanation of all charges

✅ Comparison of banks & NBFCs

✅ Negotiation on fees & interest

✅ Faster approvals

✅ No hidden surprises

We help you choose a home loan that’s truly affordable, not just attractive on paper.

FAQs – Hidden Charges in Home Loans

Q1. Are all home loan charges mandatory?

No. Some charges are negotiable or optional.

Q2. Can DSAs help reduce hidden charges?

Yes. DSAs often get fee waivers or discounts.

Q3. Do floating-rate loans have fewer charges?

Generally, yes—especially for prepayment.

Planning a Home Loan? Get Expert Help Today 🏡

📞 Free eligibility & cost check

📊 Transparent comparison

⚡ Best home loan deals

👉 Contact WERISE DSA today and avoid costly home loan mistakes!

5 Comments

Juliet4021

Partner with us and enjoy high payouts—apply now!

Ethan649

Share our link, earn real money—signup for our affiliate program!

Aniya2167

Join our affiliate community and maximize your profits!

Leah953

Turn referrals into revenue—sign up for our affiliate program today!

Carrie3625

Become our partner now and start turning referrals into revenue!